")

")

")

")

")

")

")

")

— Which Option Is Best for You?")

— How Interest Rates Really Work and What Affects Your Deal")

Introduction

UK mortgage rates have gone through significant volatility over the past few years, driven by inflation spikes, Bank of England base rate changes, and global economic instability. As we move through 2026, many borrowers are asking the same question: what happens next?

This article breaks down the UK mortgage rate forecast for 2026–2028, what factors will influence rates, and how homeowners can prepare.

Current Mortgage Rate Environment (2026)

The UK mortgage market in 2026 is characterised by:

- Moderating inflation compared to previous peaks

- Gradual stabilisation of the Bank of England base rate

- Strong lender competition

- More cautious affordability checks

While rates are no longer at emergency highs, they remain above historic lows seen in the 2010s.

Key Factors That Will Shape Future Mortgage Rates

1. Inflation Trends

Inflation remains the single most important driver.

- Rising inflation → higher interest rates

- Falling inflation → rate cuts become possible

The Bank of England prioritises keeping inflation near its target level, even if it slows economic growth.

2. Bank of England Base Rate Policy

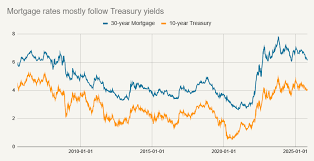

The base rate directly influences lender pricing.

i=r+m

Where:

- i = mortgage interest rate

- r = base rate

- m = lender margin

Even small base rate changes can significantly impact mortgage affordability.

3. Swap Markets and Investor Expectations

Mortgage lenders don’t just react to current rates—they price in future expectations using swap markets.

If markets expect cuts:

- Fixed mortgage rates may fall early

If markets expect instability:

- Rates remain higher for longer

4. Government Fiscal Policy

Tax decisions, spending plans, and housing policy can all influence inflation and borrowing costs.

2026–2028 Mortgage Rate Forecast (General Outlook)

2026 (Current Phase)

- Gradual stabilisation

- Slight downward pressure on fixed rates

- Competitive lender pricing

2027 Outlook

- Potential moderate rate cuts if inflation stays controlled

- Increased affordability for new borrowers

- More remortgage opportunities

2028 Outlook

- Possible return toward “normalised” interest rate environment

- Less volatility compared to early 2020s

- Stronger emphasis on borrower credit strength

What This Means for Homeowners

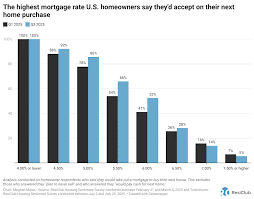

If you already have a fixed mortgage:

You are protected until renewal, but future remortgage rates matter.

If you are buying now:

Locking in a stable rate may still be wise if uncertainty remains.

If you are on a variable rate:

You are most exposed to short-term market changes.

Strategic Advice for 2026–2028

- Don’t try to “time the market” perfectly

- Focus on affordability, not speculation

- Fix rates if stability is important

- Remortgage early before SVR exposure

Conclusion

UK mortgage rates are expected to remain dynamic through 2026–2028, but extreme volatility may gradually reduce. Borrowers who plan ahead, monitor inflation trends, and choose the right mortgage structure will be best positioned.