")

")

")

")

")

")

")

")

— Which Option Is Best for You?")

— How Interest Rates Really Work and What Affects Your Deal")

Introduction

Getting the lowest mortgage rate in the UK can save borrowers tens of thousands of pounds over the lifetime of a loan. In 2026, with rates still influenced by inflation trends and Bank of England policy, lenders are competing more aggressively—but only well-prepared borrowers get the best deals.

This guide explains exactly how to secure the lowest possible mortgage rate in the UK, whether you are a first-time buyer, home mover, or remortgaging homeowner.

What Determines the Lowest Mortgage Rate?

Lenders don’t offer the same rate to everyone. Instead, pricing is based on risk.

The key factors include:

- Deposit size (Loan-to-Value ratio)

- Credit score

- Employment stability

- Property type

- Debt levels

- Mortgage term length

Even small improvements in these areas can significantly reduce your rate.

Step 1: Increase Your Deposit (Biggest Impact)

One of the strongest influences on mortgage rates is your loan-to-value (LTV) ratio.

Example:

- 95% LTV → Highest rates

- 90% LTV → Slightly better

- 75% LTV → Competitive rates

- 60% LTV → Lowest available rates

A larger deposit reduces lender risk, which directly lowers your interest rate.

Step 2: Improve Your Credit Score Before Applying

UK lenders heavily rely on credit scoring systems.

To improve your score:

- Pay all bills on time

- Reduce credit card balances below 30%

- Avoid applying for multiple loans

- Check your credit report for errors

Even a moderate score improvement can unlock better mortgage tiers.

Step 3: Choose the Right Mortgage Type

Different mortgage types come with different pricing:

- Fixed-rate mortgages (stable, often slightly higher starting rate)

- Tracker mortgages (can be cheaper initially but variable risk)

- Offset mortgages (can reduce interest using savings)

In 2026, fixed-rate deals remain the most popular due to market uncertainty.

Step 4: Compare Lenders (Never Accept the First Offer)

UK mortgage pricing is highly competitive.

Different lenders may offer:

- Different risk appetite

- Different credit models

- Different promotional rates

Using brokers or comparison tools often reveals significantly better deals than high-street banks alone.

Step 5: Lock in Rates at the Right Time

Mortgage rates move daily based on:

- Swap rates

- Inflation expectations

- Market sentiment

When rates appear to be rising, locking early can save thousands.

Step 6: Reduce Debt Before Applying

High existing debt affects affordability calculations.

Lenders look at:

- Credit card balances

- Personal loans

- Car finance

Reducing debt improves affordability scoring and can improve rate offers.

Step 7: Consider a Mortgage Broker

A broker can:

- Access exclusive lender deals

- Match you with suitable lenders

- Improve approval chances

Many of the lowest rates are not available directly to the public.

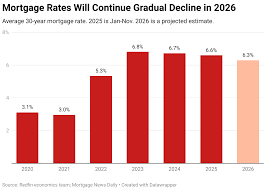

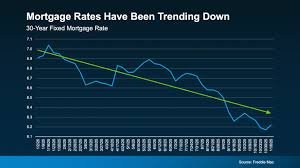

UK Mortgage Rate Trends in 2026

The UK mortgage market is currently shaped by:

- Stabilising inflation

- Gradual base rate adjustments

- Strong lender competition

This environment rewards prepared borrowers more than ever.

Conclusion

The lowest mortgage rate in the UK is not automatically offered—it is earned through preparation, financial strength, and smart lender selection.

By improving your deposit, credit profile, and lender comparison strategy, you can significantly reduce your long-term mortgage cost.