")

")

")

")

")

")

")

")

— Which Option Is Best for You?")

— How Interest Rates Really Work and What Affects Your Deal")

Introduction

UK mortgage rates are one of the most important financial factors for homeowners, first-time buyers, and property investors. In 2026, understanding how these rates are set is more important than ever, especially with ongoing changes in inflation, Bank of England policy, and lender competition.

This guide breaks down exactly how UK mortgage rates work, what influences them, and how borrowers can position themselves to secure better deals.

What Are Mortgage Rates?

A mortgage rate is the interest charged by a lender when you borrow money to buy property. It is usually expressed as an annual percentage rate (APR) or a nominal interest rate.

Even a small difference in rate — for example 4.5% vs 5.0% — can mean thousands of pounds over the lifetime of a mortgage.

The Main Driver: Bank of England Base Rate

The most influential factor behind UK mortgage rates is the Bank of England base rate.

When the base rate increases:

- Lenders face higher borrowing costs

- Mortgage rates typically rise

- Monthly repayments increase

When the base rate decreases:

- Lenders can borrow more cheaply

- Mortgage rates usually fall

- Mortgage affordability improves

However, mortgage rates do NOT move in perfect sync with the base rate — lenders also price in risk, competition, and market expectations.

Fixed vs Tracker vs Variable Rates

UK mortgages generally fall into three categories:

1. Fixed Rate Mortgages

- Interest rate stays the same for a set period (2, 3, 5, or 10 years)

- Offers stability and predictable payments

- Popular when rates are expected to rise

2. Tracker Mortgages

- Directly follow the Bank of England base rate

- Usually “base rate + margin”

- Monthly payments can go up or down

3. Standard Variable Rate (SVR)

- Set by the lender

- Often higher than fixed/tracker rates

- Used after initial deal ends

What Really Influences Mortgage Rates in 2026?

1. Inflation Levels

High inflation usually forces the Bank of England to increase interest rates to slow the economy.

2. Swap Rates (Hidden Driver)

Lenders use “swap rates” to price mortgages. These reflect long-term market expectations of interest rates.

3. Lender Competition

If many lenders compete for borrowers, rates often become more attractive.

4. Loan-to-Value (LTV)

Lower deposits = higher risk = higher rates

Example:

- 90% LTV = higher interest rate

- 60% LTV = lower interest rate

5. Credit Score and Financial Profile

Borrowers with strong credit histories often access better rates.

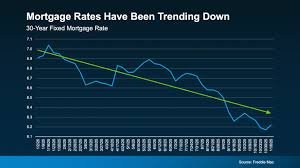

Why Mortgage Rates Change Even Without Base Rate Changes

Many borrowers are confused when mortgage rates rise or fall even when the Bank of England does nothing.

This happens because lenders price mortgages based on:

- Expected future rate changes

- Inflation forecasts

- Bond market movements

So, mortgage rates are often forward-looking, not reactive.

How to Get the Best Mortgage Rate in the UK

Improve Your Credit Score

- Pay bills on time

- Reduce credit card balances

- Avoid unnecessary borrowing

Save a Larger Deposit

- 10% vs 20% deposit can dramatically change your rate

Compare Lenders

Different banks price risk differently — comparison is essential.

Consider Fixed Deals During Uncertainty

When rates are unstable, fixed deals provide protection.

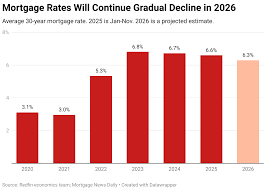

Future Outlook for UK Mortgage Rates

In 2026, analysts expect mortgage rates to remain sensitive to:

- Inflation trends

- Government fiscal policy

- Global economic stability

While sharp spikes may reduce, volatility is likely to remain.

Conclusion

UK mortgage rates are shaped by a combination of base rates, inflation, lender risk models, and market expectations. Understanding these factors gives borrowers a major advantage when choosing the right mortgage deal.

Whether you’re buying your first home or remortgaging, knowledge of how rates are formed can save you significant money over time.