")

")

")

")

")

")

")

")

— Which Option Is Best for You?")

— How Interest Rates Really Work and What Affects Your Deal")

Introduction

Choosing between a fixed or variable mortgage is one of the most important financial decisions UK borrowers face. Each option comes with advantages and risks, and the right choice depends on interest rate trends, personal finances, and risk tolerance.

In 2026, with fluctuating UK interest rates, this decision has become even more critical.

What Is a Fixed-Rate Mortgage?

A fixed-rate mortgage locks your interest rate for a set period.

Key Features:

- Monthly payments remain unchanged

- Usually lasts 2–10 years

- Protects against interest rate rises

Advantages:

- Predictable budgeting

- Stability during economic uncertainty

- Peace of mind if rates rise

Disadvantages:

- Can be slightly more expensive initially

- No benefit if interest rates fall

- Early repayment charges often apply

What Is a Variable-Rate Mortgage?

Variable mortgages change based on market conditions or lender decisions.

Types:

- Tracker mortgages (linked to Bank of England base rate)

- Standard variable rate (set by lender)

Advantages:

- Potentially lower initial rates

- Can benefit from falling interest rates

- More flexible in some cases

Disadvantages:

- Monthly payments can rise unpredictably

- Harder to budget long-term

- Exposure to economic volatility

Fixed vs Variable: The Real Cost Difference

The biggest difference is risk distribution:

| Factor | Fixed Rate | Variable Rate |

|---|---|---|

| Payment stability | High | Low |

| Risk exposure | Low | High |

| Initial cost | Slightly higher | Often lower |

| Benefit from rate drops | No | Yes |

Even a 1% rate change can significantly impact total repayment over time.

When Fixed Rates Make More Sense

Fixed mortgages are usually better when:

- Interest rates are rising or unstable

- You prefer financial predictability

- You are on a tight monthly budget

- You are buying your first home

In uncertain economic conditions, fixed rates act as protection against volatility.

When Variable Rates Make More Sense

Variable mortgages can be beneficial when:

- Interest rates are expected to fall

- You can handle payment fluctuations

- You plan to sell or remortgage soon

- You want to take advantage of short-term savings

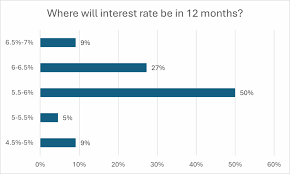

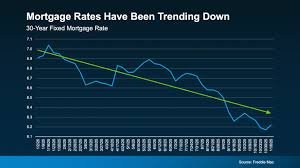

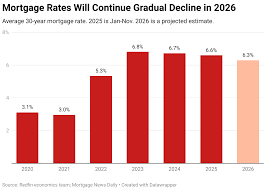

The 2026 UK Mortgage Climate

In 2026, the UK mortgage market remains influenced by:

- Inflation stabilisation efforts

- Bank of England rate adjustments

- Global economic pressure

This creates a mixed environment where neither fixed nor variable is universally superior.

Instead, choice depends heavily on individual risk appetite.

Hybrid Strategy: A Smart Middle Ground

Some borrowers use a hybrid approach:

- Start with a fixed rate for stability

- Switch or remortgage later if conditions improve

This strategy balances security and flexibility.

Expert Insight: What Most UK Borrowers Choose

Historically in the UK:

- Fixed-rate mortgages dominate (especially 2–5 year terms)

- First-time buyers prefer stability

- Investors sometimes prefer variable for flexibility

Final Verdict

There is no single “best” mortgage type. Instead:

- Choose fixed if you want stability and protection

- Choose variable if you want flexibility and risk tolerance

The right decision depends on your financial situation and market expectations.

Conclusion

Understanding the difference between fixed and variable mortgages is essential for making informed financial decisions in the UK housing market.

In uncertain economic conditions like 2026, the best mortgage is not just about the lowest rate — it’s about the right balance between risk and security.